Late payment is an ongoing problem for small businesses across the UK. Almost half (46 per cent) of small businesses have been owed between £10,000 and £20,000 in late payments, according to Simply Business research.

For 42 per cent of businesses, late payments take between four and nine days to be settled on average, while data from the government suggests that the average small business has nine overdue invoices at any one time.

That’s why a late payment letter, also known as an ‘outstanding payment letter’, ‘debt recovery letter’ or ‘overdue invoice letter’, is a handy tool to have on file.

Read on for tips on how to write a letter for late payment – whether it’s a polite nudge, clear reminder, or a final strong letter for outstanding payment.

To make the process even easier, you can also download our late payment letter template to help recover an overdue invoice.

The following guide covers:

When should I send an outstanding payment letter?

You’ve received a purchase order from a customer, sent the items, and issued an invoice – yet you haven’t received payment. What do you do now?

Most of the time, late payment can be easily settled with a quick overdue invoice email to your customer, gently reminding them that they haven’t paid.

When that doesn’t work, however, or you get no response, a letter in the post can help to formalise the situation. Make sure you’ve got an up-to-date address for correspondence, and keep a copy (and record) of everything you send and receive.

To get you started, here’s what an initial outstanding payment letter should include, when to send a ‘nudge’ – and if that fails, what to write in a strong letter for outstanding payment.

How to write a late payment letter

Hopefully you’ll only ever need to send one polite nudge for late payment. But if not, you may need a couple of other templates to get the message across, including a firm reminder and a final notice letter.

These are the basic details each letter needs to include:

Late payment polite nudge for an overdue invoice

- your company name and address

- recipient’s name and address

- today’s date

- a clear reference and/or any account reference numbers

- the amount outstanding

- original payment due date

- a brief explanation that no payment has been received

- next steps (you could give the recipient the opportunity to contact you and/or pay within a specific number of days)

- payment options

- reference to your payment terms

Late payment firm reminder/late payment charges letter

- your company name and address

- recipient’s name and address

- today’s date

- a clear reference and/or any account reference numbers

- the amount outstanding

- a reference to your polite nudge or last communication

- a brief explanation that payment is still outstanding, and any charges that may be added in line with your payment terms (and current government legislation)

- next steps, including a cut-off payment date

- payment options

- reference to your payment terms

Late payment final demand letter/letter before action

- your company name and address

- recipient’s name and address

- today’s date

- a clear reference and/or any account reference numbers

- the breakdown of the total amount outstanding, including any additional charges/interest

- a reference to your reminder letters or last communication

- a brief explanation that payment is still outstanding and now in breach of your payment terms

- explanation of any further costs added

- next steps, including a final cut-off date and consequences for failure to pay (this will depend on your debt recovery arrangements)

At this stage, it’s important to think about whether you’re making a formal statutory demand. This gives someone 21 days to pay the debt or reach an agreement with you to pay. If they don’t, you can apply to the courts to bankrupt your debtor or wind up their company, but this can be a costly process – so consider whether you’ve exhausted all of your options.

Read more about making a statutory demand at gov.uk, as there are specific forms that you need to use.

If you’re not making a statutory demand, then this letter can simply be a strong letter for outstanding payment. Still, if you don’t receive a response, then a statutory demand may be necessary.

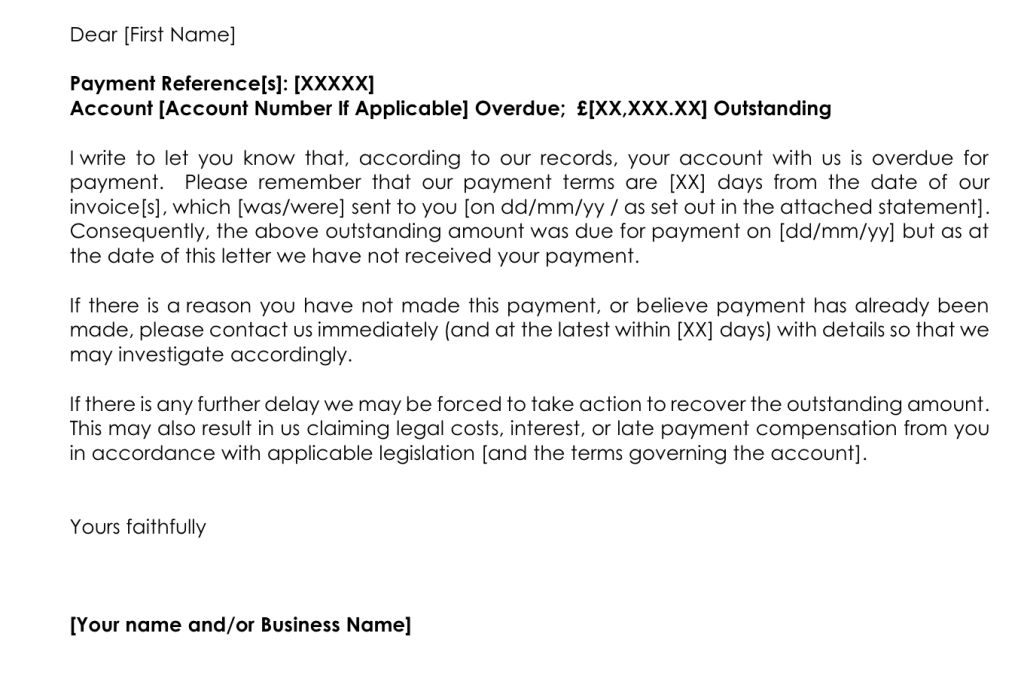

Debt recovery letter template

Here’s a late payment letter template, giving a reminder of the amount outstanding and due date, plus next steps.

You’ll need to edit this according to your business and circumstances. For example, it might be more appropriate to mention a specific overdue invoice (including the invoice number and any other relevant details), rather than an overdue account balance.

You can also amend this template to turn it into a firm reminder or a strong letter for outstanding payment, according to the steps above. It depends on which stage of the process you’re at.

How to work out late payments

Did you know you can charge interest on overdue invoices?

The Small Business Commissioner has a late interest payment calculator you can use to work out how much interest you can charge on top of the outstanding balance.

To use the late payment calculator to work out interest, you’ll just need to input the following information:

- payment terms (usually 30 days)

- invoice date

- date invoice was paid (if it has been paid)

- total amount on the invoice

Remember, this article is just a guide, and it’s always worth seeking professional legal advice.

What is the Late Payment Act 1998?

The Late Payment of Commercial Debts (Interest) Act 1998 allows you to charge interest on overdue payments from other businesses.

You can claim interest at eight per cent above the Bank of England base interest rate (currently 5.25 per cent), as well as compensation of up to £100 for each invoice depending on how much is owed:

- £40 for invoices up to £999

- £70 for invoices between £1,000 and £9,999

- £100 for invoices over £10,000

The law also allows businesses to claim for ‘reasonable costs’ if the cost of recovering the debt is more than the compensation.

You can charge interest and claim compensation as soon as the payment is overdue, as set out by your payment terms or agreed credit period.

Late payment interest example

If you’re owed £3,000 by a client, you could charge interest at 13.25 per cent (eight per cent above the current base rate of 5.25 per cent).

This would work out as £397.50 annually or £1.09 a day.

To work out how much the client owes in interest, you can multiply the daily amount by the number of days the payment is overdue.

For example, if the payment was 20 days overdue, you’d be owed £21.80 in interest.

As the invoice is between £1,000 and £9,999, you’d also be able to claim compensation of £70.

Tips for preventing late payment

There are some things you could try to minimise the chance of late payment.

Make your payment terms clear – your invoice should include details of how to pay, your bank details, and clearly state the date they have to pay by.

Invest in accounting software – this can automate reminders to prompt payment, saving you time on chasing up unpaid invoices.

Consider credit checks – you could look into your customer’s credit rating before working with them to help give you peace of mind.

Try using ‘proforma’ invoices – for new customers you could ask them to arrange payment before you supply the products or services to build trust that they’ll pay on time.

What is the government doing to prevent late payments?

In 2023, the government launched a Cash Flow and Prompt Payment review, with the aim of reducing the payments owed to small businesses.

The government’s plans include strengthening the existing Prompt Payment Code and giving the Small Business Commissioner more powers to crack down on late payments.

It also promised to provide more advice to small businesses on how to negotiate payment terms and encourage more businesses to adopt digital payment technology.

How legal expenses insurance can help

If you have legal expenses insurance as part of your Simply Business policy, you have access to a number of useful services through DAS Businesslaw (you’ll just need your voucher code found in your policy documents to register).

DAS has a legal advice helpline, available whether you’re facing a serious legal issue or just want to check something with an adviser. They also offer a range of legal templates and guides to help you with managing tenancies.

More useful articles for small business owners

- How to write an invoice

- A guide to bookkeeping for small businesses

- What is a statement of account?

- What type of business insurance do I need?

Looking for self-employed insurance?

With Simply Business you can build a single self employed insurance policy combining the covers that are relevant to you. Whether it’s public liability insurance, professional indemnity or whatever else you need, we’ll run you a quick quote online, and let you decide if we’re a good fit.

This block is configured using JavaScript. A preview is not available in the editor.