Feel simply the best about your business insurance.

Get a quote in minutes and join over one million business and landlord customers.

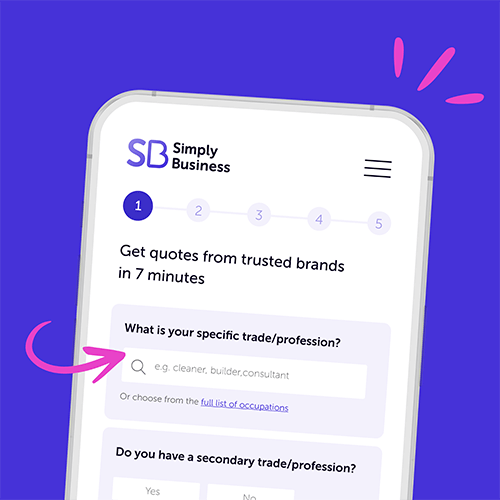

What type of business do you want to insure?

Compare quotes from leading brands

Rated 4.6/5 based on 40k reviews

Chosen by over one million small business and landlord customers

With insurance for over 1,500 trades, and 9/10 customers rating us ‘good’ or ‘excellent’ on Feefo, you can get tailored quotes in 7 minutes. Compare quotes from leading insurers, buy, and manage your policy – all in one place.

Small businesses deserve our best

From freelancers to shop owners and tradespeople to landlords, it’s our mission to make small business owners feel simply the best about their insurance.

Whether you’re looking to compare quotes from leading insurers, or get an online quote in minutes, we’ve got you covered when it comes to landlord and business insurance.

Not quite ready to buy?

Sign up for a reminder to get your insurance with Simply Business and we’ll send you a £25 gift card after you buy.

We’ll then send you a link to buy insurance at the right time for you. To get your gift card, you’ll need to use this link when buying your policy.

If your policy is still in place (with up to date payments) three weeks after your start date, we’ll send you an email with instructions on how to redeem your reward within 45 days. Terms and conditions apply.

Insurance tailored to bigger businesses

Cover that’s designed to meet the needs of all SMEs. Our customer-first approach makes it easy to get the right level of cover that protects your business and your people, giving you peace of mind.

Get cover for all of your commercial needs with tailored, reliable, and comprehensive insurance that’s available online or over the phone with our expert team.

5 trending products to sell in 2025

Over on our Knowledge centre, we dig into the data to uncover some of the most popular products to sell in 2025. Could you find your next best-seller?

Landlord insurance for over 300,000 customers

Thousands of landlords trust us with their insurance, giving them the peace of mind that their investment is protected.

Choose from a range of key covers and build a landlord insurance policy to suit your needs. Whether you’re looking for buildings or contents insurance, or cover for legal expenses or loss of rent, you can compare quotes from leading insurers all in one place.

Get your tailored landlord insurance quote in minutes and only pay for the cover you need.

Get support from UK-based insurance experts

Excellent customer service is at the heart of everything we do at Simply Business.

Whether you want to make a change to your policy or discuss a claim, we have a team of UK-based experts who can help you feel the best about your insurance.

They’re on hand to answer your questions and help make protecting your business as simple as possible.

Our expert team is just one part of our 24/7 service, which allows you to manage your insurance in whatever way works for you.

Don’t take our word for it, here’s what our customers say about us…

Exceptional 4.6/5

40k reviews

What we do

As one of the UK’s biggest business insurance providers, we specialise in covers like professional indemnity insurance and employers’ liability insurance. We cover landlords too, offering insurance like tenant default insurance and rent guarantee insurance.

How it works

Whether you’re a cleaner or tradesperson, it’s quick to buy insurance. Answer a few questions and we’ll show you quotes from leading insurers in minutes. It’s easy to buy a range of covers, from public liability insurance to business equipment protection.

Why we do it

We know that every small business or rental property is unique, which means your insurance should be too. We aim to take the hassle out of buying a policy, helping you focus on your big dreams.